Account Administrators

Configuring SOD and credit as an account administrator

As an account administrator, you can configure position reset times, SOD functionality, and the daily credit limit for the accounts you are managing. Credit loss adjustment settings are grayed out and can only be set by the company administrator.

Note: The Update account position settings account administrator checkbox must be checked to perform these tasks.

To configure position settings and credit limits:

- Click Accounts in the left navigation pane and select an account in the data grid.

- Click the SOD/Credit tab for the selected account.

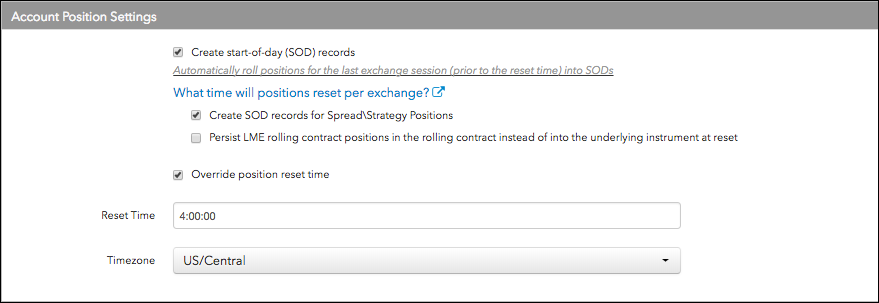

- In the Account Position Settings section, you can configure the following settings:

- Create start-of-day (SOD) records — Determines whether position records (SODs) are generated for the prior exchange session at the daily reset time. This setting applies even if credit risk is disabled. At the account-level, this setting is enabled (checked) by default. Uncheck to disable this setting.

- Create SOD records for Spread\Strategy Positions — Determines whether position records (SODs) are generated for spreads/strategies for the prior exchange session at the daily reset time. When this option is checked (enabled), a separate SOD is generated that shows the position of the spread/strategy itself and not just the outright legs. This setting is configurable and applies even if credit risk is disabled. At the account-level, this setting is disabled by default. If enabled on the account, traders assigned to this account must enable the Display spread/strategy positions option in the Global Settings | General tab in the Trade application in order to view their spread/strategy positions. Check to enable this setting.

Persist LME rolling contract positions in the rolling contract instead of into the underlying instrument at reset — Determines whether LME rolling contracts are rolled into their underlying positions or into their new rolling contract at the daily reset time.

By default this option is unchecked, and a position in an LME rolling contract is listed in its underlying contract after the daily reset. When checked, a position in an LME rolling contract is rolled forward into the new LME rolling contract.

By default this parameter is unchecked. It can only be checked when Create start-of-day (SOD) records is checked, and is cleared when Create start-of-day (SOD) records is unchecked.

Override position reset time — Determines your own reset time for the account. Uncheck this option to automatically use the exchange's position reset time. To choose a single time for position reset, check the override option and set a time and timezone.

Note: The parent level override setting applies to all child accounts. If Override position reset time is enabled for a parent account, then the child account cannot be set to a reset time that is different from the parent account's position reset time.

- If override is enabled, enter your own specific Reset Time and Timezone for the account's position reset.

This sets the required position reset time. Positions reset regardless of whether credit limits are applied to the user or whether the Create start-of-day (SOD) records option is checked.

By default, the reset time is 0:00:00. The timezone is not set by default, but is required before you can save any changes. This allows for a seamless, 24 hour trading cycle that doesn't have to align with the exchange rollover times by region where matching occurs. The position reset time is configurable and adhered to even if the credit risk setting is disabled for an account or user.

When a session resets, the following occurs:

- Fills from the previous exchange session are removed. Historical fills are retrievable but not part of the current session's position fills.

- If the “Create start-of-day (SOD) records” and/or "Create SOD records for Spread\Strategy Positions" option is checked, fills are replaced with SOD records per contract priced at the previous exchange settlement. Otherwise, no record or a record of zero is generated.

- Fills that occurred since the current exchange session remain.

- Working orders remain.

- If “Credit Check” is enabled and the Rule is to apply P&L, then P&L from previous exchange sessions is added to the credit check; and orders, fills, and SODs are considered in the credit check.

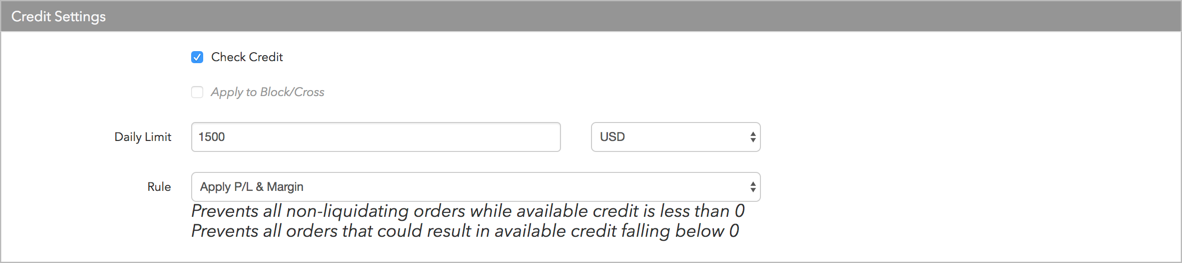

- In the Credit Settings section, configure the following:

- Check Credit — Check (enable) this checkbox to apply credit limit checks to all orders.

- Apply to Block/Cross Orders — Check this checkbox to apply the credit limits to all Block or Cross orders. If unchecked, user credit does not apply to these orders.

- Daily Limit — Determines the daily credit amount the account can have during a given trading session. Enter a number (zero or greater). Select a currency for the credit limit from the drop down menu next to this field.

- Rule — Select one of the following methods for calculating available credit:

- Apply P/L — Uses the P/L formula to determine available credit. If selected, then any profits or losses (realized and unrealized) that accrue during the day are added or subtracted from the account's available credit. If this is checked, then the credit limit acts as a pure daily loss limit. Prevents all non-liquidating orders while available credit is less than 0.

- Apply Margin Limit — Considers product margin limits set by the company when determining available credit per trading session. This setting deducts product margin from the account's available credit based on the worst case net positions in various products. Prevents all orders that could result in available credit falling below 0.

Apply P/L & Margin — If margin and P/L are both included in the credit check per trading session, then available credit = daily credit +/- P/L - margin. Select this option as a balance if credit is updated daily in one of two ways: Manually by your firm, or automatically marking-to-market by adding yesterday's P/L to today's credit and representing yesterday’s position at the settlement price.

Upon entering an order, margin is calculated on a worst-case basis, applying outright margin to working uneven spreads, outright orders, and worst-case outright positions. Spread/strategy margin is applied to working even spreads and synthetic spread positions (e.g., a 1-lot long position in Sep 16 and a 1-lot short position in Dec 16 only requires one times the current spread margin value). If a new order would cause available credit to drop at or below zero, then the order is rejected unless the only possible result of the order being filled would be to reduce the position in all affected contracts without increasing the gross or net position of any products (requires Trade out allowed enabled).

- Apply pre-trade SPAN margin — Incorporates both P/L and margin where margin values are calculated via portfolio risk calculation using values supplied by the exchange. Requires Cash Balances values to be set. Does not support all exchanges. For more details please see Pre-Trade Portfolio Risk.

- Click Save Changes