Electronic Eye

Electronic Eye reference

This reference describes the settings available for the Electronic Eye widget and the fields you can use to create filters.

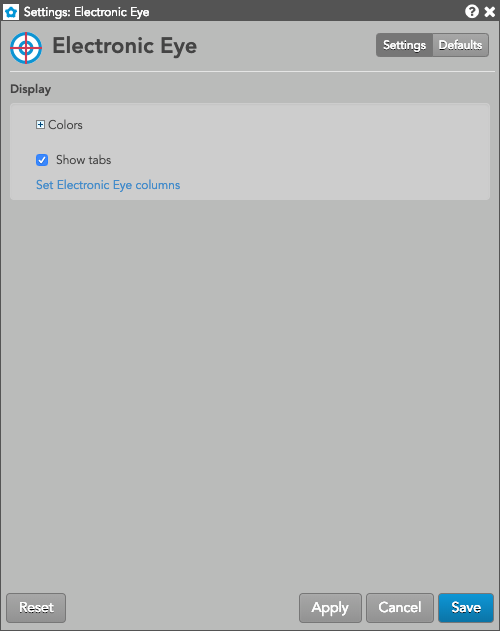

Display settings

- Grid font size: Adjust the font size to suit your preferences and use bold text, if desired.

-

Colors: Allows you to customize or change the cell and column colors available in the widget.

- Show tabs: Check to show tabs at the bottom of the widget. Uncheck to hide tabs.

- Set Options Electronic Eye columns: Select the columns you want shown in the Options Electronic Eye.

Options Electronic Eye column descriptions

| Column | Description |

|---|---|

| Instrument | Options instrument |

| C/P | Whether the instrument is a call or put option. |

| Strike | Shows the underlying Futures contract price at which a holder can exercise their option to buy or sell the contract. The strike column reflects the range of the day by shading the strike. The high / low line indicators as seen on MD Trader® are displayed in the strike column relative to their position. |

| DTE | Number of days until the option expires. |

| Expiration Type | Type of expiration (e.g. monthly, weekly) associated with the options instrument. |

| UndPx | The price of the underlying instrument at the time of the fill. |

| BidQty | The total quantity working at the bid. |

| Bid | The best market bid price. |

| Sell Edge | Difference between the best bid and the theoretical value. |

| U TV | The theoretical value of the instrument based on the user's volatility curve. |

| ATM Vol | At-the-market volatility. |

| Buy Edge | Difference between the best ask and the theoretical value. |

| Ask | The best market ask price. |

| AskQty | The total quantity working at the ask. |

| UV | User volatility values that are used for calculating theoretical call and put values. These user-defined vols are entered using the Vol Curve Manager, which fits the curve to the control points on the volatility curve. The user volatility values are a result of the fitting process. |

| UΔ | Delta calculated using the user-defined volatility. |

| IV | Implied volatility value. Implied volatilities are calculated using the midpoint of bid and ask prices. |

| IΔ | The delta calculated with the auto-fit volatility curve values provided by TT. |

| SV | Settlement volatility value, which indicates volatility calculated per strike using settlement prices. |

| SΔ | Delta calculated using the settlement volatility. |

Filter field descriptions

When creating filters, you can use the following fields in a rule.

| Field | Description |

|---|---|

| Active Delta | Call delta calculated using the active volatility curve in the Vol Curve Manager widget. |

| Active Gamma | Change in delta per change in the underlying, calculated using the active volatility curve in the Vol Curve Manager widget. |

| Active Rho | Change in options value per change in interest rate, calculated using the active volatility curve in the Vol Curve Manager widget. |

| Active Theta | Change in options value per change in time, calculated using the active volatility curve in the Vol Curve Manager widget. Also known as time decay. |

| Active TV | Theoretical value of an option calculated using the Barone-Adesi and Whaley price model with the active volatility curve in the Vol Curve Manager widget as an input. |

| Active Vega | cChange in options value per change in volatility, calculated using the active volatility curve in the Vol Curve Manager widget. |

| Active Vol | TT-calculated theoretical value based on the active volatility curve values in the Vol Curve Manager widget. |

| Ask Implied Delta | |

| Ask Implied Gamma | |

| Ask Implied Rho | |

| Ask Implied Theta | |

| Ask Implied TV | |

| Ask Implied Vega | Change in the price of the Call or Put Option for every 1% change in the volatility of the underlying Futures contract calculated using the implied Ask prices. |

| Ask Implied Vol | |

| Atm Vol | |

| Bid Implied Delta | |

| Bid Implied Gamma | |

| Bid Implied Rho | |

| Bid Implied Theta | |

| Bid Implied TV | |

| Bid Implied Vega | Change in the price of the Call or Put Option for every 1% change in the volatility of the underlying Futures contract calculated using the implied Bid prices. |

| Bid Implied Vol | |

| Buy Edge | |

| DTE | Number of days until the options instrument expires |

| Expiration Type | Type of expiration, such as monthly or weekly |

| Market Ask Px | |

| Market Ask Qty | |

| Market Bid Px | |

| Market Bid Qty | |

| Mid Implied Delta | |

| Mid Implied Gamma | |

| Mid Implied Rho | |

| Mid Implied Theta | |

| Mid Implied TV | |

| Mid Implied Vega | Change in the price of the Call or Put Option for every 1% change in the volatility of the underlying Futures contract calculated using the midpoint of the implied Bid and Ask prices. |

| Mid Implied Vol | |

| Put/Call | Whether the instrument is a put or call option. |

| Sell Edge | |

| Settlement Delta | |

| Settlement Gamma | |

| Settlement Rho | |

| Settlement Theta | |

| Settlement TV | |

| Settlement Vega | Change in the price of the Call or Put Option for every 1% change in the volatility of the underlying Futures contract calculated using the settlement prices. |

| Settlement Vol | Settlement volatility value, which indicates volatility calculated per strike using settlement prices. |

| Std. Dev | |

| Strike | Strike price for the options instrument |

| TT Delta | |

| TT Gamma | |

| TT Rho | |

| TT Theta | |

| TT TV | |

| TT Vega | |

| TT Vol | |

| Underlying Ask Px | Best ask price of the underlying instrument |

| Underlying Bid Px | Best bid price of the underlying instrument |

| Underlying Px |